Hello there! Today it's once again about P2P, to be exact, about the P2P portfolio update February 2022! February unfortunately goes down in history negatively due to the Russian invasion of Ukraine. Some P2P platforms are affected as well due to lending in both countries. Let's get started!

First comes the IRR ranking, as usual, and then a closer look at the individual platforms. I have adjusted the subdivision of the platforms once again because it has led to confusion here and there. There are the categories ‘(Re)invested‘, ‘Withdrawal phase‘ and ‘Investment expires'.

‘Strategy'

My strategy for 2022 will be adjusted to the extent that the cash flow from interest on the platforms will remain or at least only be redistributed within the platforms. The goal is to increase the investment on as many platforms as possible to such an extent that I can receive 25 EUR in interest every month (if I want to!).

IRR ranking February 2022

I've selected the 01.07.2017 as a start, as this is where I started tracking my P2P investments.

Platform | Initial investment | IRR (%) | Changes previous month (%) | Invested (EUR) | Changes previous month (EUR) |

|---|---|---|---|---|---|

19.07.2017 | 11,71 | -0,12 | 7099 | +1351 | |

30.10.2017 | 10,74 | -0,06 | 1088 | +7 | |

09.11.2017 | 6,67 | +0,01 | 1007 | +76 | |

14.05.2018 | 12,47 | -0,10 | 1062 | +6 | |

31.07.2018 | 11,71 | -0,07 | 1767 | +11 | |

11.08.2018 | 12,90 | +0,17 | 541,16 | +6,51 | |

01.02.2019 | 9,59 | +0,01 | 3566 | +26 | |

14.02.2019 | 13,07 | -0,04 | 1404 | +12 | |

20.02.2019 | 9,32 | +1,48 | 1880 | +154 | |

21.03.2019 | 8,69 | -0,02 | 13644 | -110 | |

30.03.2019 | 11,32 | -0,02 | 1235 | +9 | |

12.04.2019 | 11,69 | +0,04 | 1411 | +13 | |

17.05.2019 | 8,58 | +0,08 | 886,28 | +7,67 | |

Crowdestate | 20.05.2019 | -7,71 | +0,04 | 152,65 | -15,60 |

31.07.2019 | 3,29 | +0,17 | 5845 | -91 | |

15.02.2020 | 15,55 | -0,15 | 1105 | +10 | |

20.02.2020 | 7,42 | +0,07 | 330,94 | +2,20 | |

29.05.2020 | 4,39 | -0,50 | 598,52 | -2,85 | |

22.07.2020 | 9,80 | -0,02 | 581,41 | +4,02 | |

28.01.2021 | 10,22 | -0,86 | 110,07 | 0 | |

21.03.2021 | 13,57 | -0,56 | 609,45 | -94,78 | |

10.06.2021 | 13,36 | +0,11 | 478,13 | +103,89 | |

10.06.2021 | 10,60 | +0,41 | 681,26 | +6,22 | |

23.07.2021 | 10,80 | +0,31 | 526,95 | +4,94 | |

15.11.2021 | 17,97 | -0,06 | 65,32 | +0,78 | |

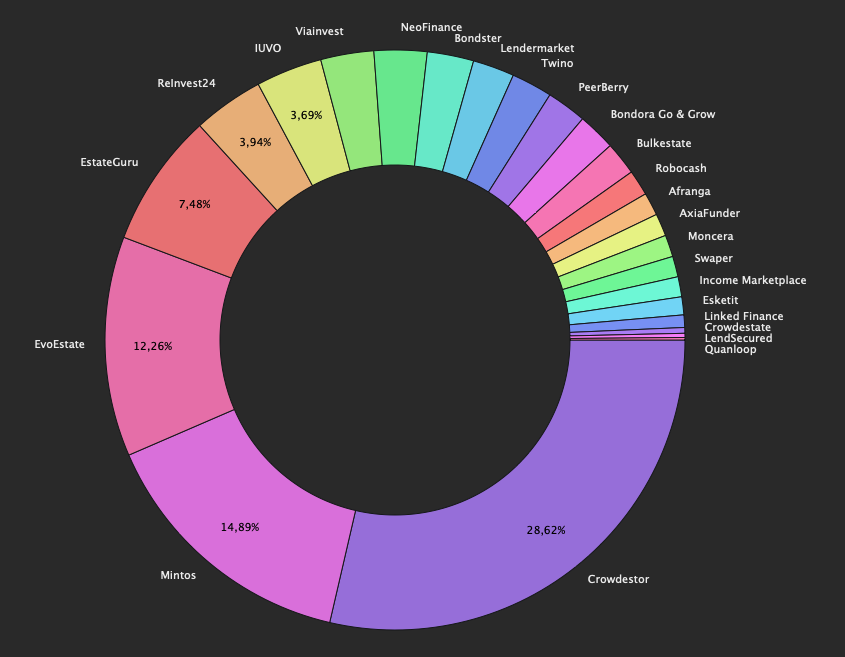

28.02.2022 | +2,22 | +0,20 | 47686 | +2445 |

Platforms

(Re)investing

I continue to reinvest on the following platforms and plan to increase the investment in a targeted manner in order to maintain a monthly cash flow of at least EUR 25 or even increase it beyond that.

P2P (Buy-back)

![]()

As planned, I deposited the money withdrawn for testing again. And in the course of this, the conservative strategy was immediately terminated again. The interest rates are rising again and I have too many loan providers in the conservative strategy, which are facing challenges. I will publish a list of my selected loan providers in the next update, but I am strongly oriented to the P2P platform rating premium, which you can find further down in the blog post. The IRR at the end of February was 11,71% with 7.099 EUR invested.

Even if Mintos is one of my largest platforms, still 28% of my investment is questionable. Namely all pending payments and loans in recovery.

Mintos has temporarily suspended its affiliate program again.

On IUVO 1.767 EUR were invested at the end of February with an IRR of 11.71%.

Currently, 22,9% of the investment is questionable due to the Polish CBC loans.

- For IUVO there are two different offers. Unfortunately, the referral program is extremely unattractive since a few days. For the first you can contact me because unfortunately it has to be done manually, and I have to invite you. You get 1,5% cashback for investment above 1.000€. I receive 1,5% too.

- With the 2nd offer (click on the banner) I get 5€ and 2% of the investment in the first 30 days and 3% for the investment of day 31-90

![]()

At Lendermarket, the IRR went back down a bit to 15,55% in February. Due to the war and the resulting increased risk for investors, some platforms have raised interest rates. Lendermarket is now offering up to 16% again here. My investment was at 1.105 EUR at the end of February.

Because the platform is new and I ‘only' invested 1.000 EUR I won't put capital as questionable for now.

On the platform you get 1% cashback if you are using my link*. Currently, in total up to 17%! My reward is 5€ onetime + 1,5%

![]()

Swaper remains opaque as always, but is running. At the end of February, the IRR was 12,90%. All this with an investment of 547,67 EUR.

Because I just have a few Euros invested, I won't put it as questionable for now.

If you use my link* my reward is onetime 5€ + 2% cashback for 90 days.

Twino is the first platform in today's blog post with quite a large exposure to Russia, including loans with currency impact. The IRR at the end of February was 10,74% with 1.088 EUR invested. As of today, Twino has informed investors how the Russian loan portfolio will be handled. Russian loans are to be extended to the maximum, which currently means six extensions plus 61 days. Interest continues to accrue and is paid monthly. So the platform is buying itself some time.

For almost 4 years, the platform has been running so solidly that I don't considered my investment questionable. And then came this war. As of today, all Russian loans are questionable.

Here* you can register. If you invest 100€ we both are rewarded with a bonus of 15€.

At Moncera, 581,40 EUR was invested at the end of February with an IRR of 9,80%.

1 1/2 years of investment in Moncera and the still small investment amount do not let me consider this investment as questionable.

If you use my Moncera link* we both receive 0,5% cashback on all deposits made by you in the first 60 day.

In February, there were actually many new loans. It's just a shame that I had already withdrawn 100 EUR and moved it on another platform. In total, there were 609,45 EUR on the platform at the end of February with an IRR of 13,57%.

As always with new platforms, I test the entire platform first with a small amount and share my observations. Due to the still small amount invested, the investment itself is not questionable.

If you are interested in Afranga, you are welcome to use my link* and support my blog. Unfortunately, only I receive 1% cashback. Prerequisite for this, you invest >500 EUR.

Esketit was precisely this candidate to which I had reallocated the funds from Afranga. The IRR at the end of February was 13,36% with 478,13 EUR invested.

Of course, this is also a test balloon. I look at the whole thing over a longer period of time before I strongly increase the investment. Nevertheless, the investment should be increased further. Due to the low investment amount, I do not see the investment as such as questionable.

For the curious, there is 1% cashback on the investment for the first 90 days at Esketit with my link*. I also receive this as compensation + one-time 5€.

![]()

Robocash had 681,26 EUR invested at the end of February with an IRR of 10,60%. After the war started, many investors panicked because Robocash is a Russian platform. However, it is headquartered in Croatia and they only lend minimally in Russia (not through the platform). For me, this was therefore no reason to act hastily. By the way, the platform has been on the market for 5 years!

Due to the increase, but still a small investment amount, I do not see the investment as such as questionable. Moreover, Robocash has quite a long track record.

If you are interested in Robocash, you can use my link* and get 1% cashback until April 30, 2022. As compensation, I get 1% cashback as well after 90 days and a one-time 5€.

On Income Marketplace 531,89 EUR were invested at the end of February with an IRR of 10,80%.

500€ is of course not a small amount for a test balloon, but without some skin-in-the-game experience reports are not authentic. I do not see the investment as questionable.

If you want to test the platform there is 1% cashback for you if you use my link* and use the code CLHOFU during registration. I receive 1% too + one-time 20€.

![]()

PeerBerry has the largest exposure to Ukrainian and Russian loans. About 50% of the total loan portfolio is affected. However, the CEO has been very honest and transparent about the situation. The plan is to balance everything within 24 months. 50% of the company's profits are to be used for this purpose. My IRR at the end of February was 12,47% with 1.062 EUR invested. The interest rates were increased accordingly for many loan originators on the platform.

One of the most solid platforms for over three years! Also here until now. A war is of course a worst case scenario, which is why about 60% of my portfolio is questionable.

A while ago PeerBerry introduced a loyalty bonus, but with high requirements:

- 0,5% for 10.000€

- 0,75% for 25.000€

- 1% for 40.000€

If you use my PeerBerry* link, I'll receive 5€ + 1% from investments for 60 days.

Bondster also has some Russian loan originators on board, namely Kviku and Lime. These are also no longer offered on the primary market, but on the secondary market. The IRR at the end of February was 11,32% with 1.235 EUR invested.

I still see Bondster as a young platform and even if the collection of Polish loans works out very well, I see 30% of the investment as questionable.

There is a 1% cashback after 30 days at Bondster*. I receive 2%.

![]()

The IRR at Viainvest was 11,69% in February on an investment of 1.411 EUR. In fact, there is nothing more to report at Viainvest.

In my opinion, Viainvest is very solid and therefore I do not consider my investment questionable.

For the start at Viainvest* there is a 15€ bonus. For this only 50€ need to be invested. I'm also rewarded with 15€ if you register with my link.

P2B (Real estate)

![]()

At the end of February, 3.566 EUR were invested with an IRR of 9,59%. In the meantime, I am also using the Auto-Invest again.

I don't consider my invested capital to be ‘questionable'. So far EstateGuru has always ensured recovery.

At EstateGuru* there is a 0,5% cashback for 3 months. I also receive the cashback and in addition 5€.

![]()

February saw further inflows of funds into Reinvest24 and I invested in a total of five new projects. A larger one also came back successfully. The IRR at the end of the month was 9,32% with 1.880 EUR invested.

Even though Reinvest24 is still one of the younger platforms, I do not consider my invested capital to be questionable.

If you want to invest on ReInvest24*, there is a 10€ bonus for you. I'll receive 1% of the investment.

![]()

As of today, the first phase of the merger is through with some delay due to technical challenges. You can read everything important here. You can (and should) watch a Q&A with the CEOs Gustas and Audrius here. Interest at EvoEstate is *withdrawn* virtually and is available at InRento.

In total, 5.845 EUR were invested in EvoEstate at the end of February with an IRR of 3,29%. I donated one successfully repaid project directly to support Ukraine. By the way, the calculated return differs strongly from the “Net Annual Returns”, which is 10,86%, due to final maturity projects.

I welcome the merger as it brings some advantages for us EvoEstate investors.

For EvoEstate there is a 0,5% cashback for 6 months with this link*. I get 0,5% too and one-time 5€. Currently there is also 1.5% cashback for investments on the primary market!

Alternatively, you can also register via my InRento* link, for this you will receive a 20€ bonus, while I receive 50€. However, the minimum investment is then 500€, which is why the upper variant is to be preferred!

![]()

886,28 EUR are invested currently in Bulkestate, … as usual, maybe more or less. The IRR was 8,58% at the end of February.

I think about 5% of the capital is questionable, because of the two delayed projects and because I do not know how well the recovery is working.

If you use my link*, I'll receive 1% cashback for 180 days and one-time 5€.

P2B

![]()

At Quanloop, 65,32 EUR was invested at the end of February. The IRR is at 17,97% due to the earlier investment, but should fall quickly to a normal level.

I'm sort of continuing the experiment, only with a bit more cash, in the medium term I had in mind 500-1.000 EUR. And of course I will report about everything.

If you register with Quanloop via my link*, you will receive a bonus of 5€. I get 2,5% cashback.

![]()

In February, the IRR at Linked Finance was 7,42% with a total investment of 330,94 EUR. Projects are now available more often again.

So far, exclusively paying or already repaid projects. Therefore, I do not consider my investment questionable.

Linked Finance doesn't have an affiliate program, so there's nothing for you or me. Nevertheless, you can register here if you like.

P2P

![]()

At NeoFinance, the lack of new loans is noticeable lately, these are usually financed again very quickly. Currently 1.404 EUR are invested at NeoFinance with an IRR of 13,07%.

The return calculated by the platform is now 14,03% after an adjustment of the calculation. There is a deduction of 15% withholding tax (can be reduced to 10% by the way).

At least the 91-270 days overdue loans I have to mark as questionable even though some of them might pay in the future. I think approx. 19% of the capital is questionable in the current situation.

NeoFinance* changed and lowered their offer too. There is 1% cashback for you and me for 90 days.

P2P (Short-term)

![]() Go & Grow

Go & Grow

Go & Grow I mainly use for a small part of my cash and will also use it for my side hustle and savings for insurance payments. Because of the withdrawals from time to time and the fee of 1 EUR IRR is at 6,67%. At the end of February, the account was replenished and had 1.007 EUR invested after I needed the liquidity temporarily.

I don't think my investment here is in question. Bondora has enough leverage.

A 5€ bonus is available for you at Bondora* right after registration.

Crowdlending

LendSecured is one of the smallest investments, which should (still) change soon. At least 500 EUR should work there and earn interest. This is still the plan, but the free funds are missing. At the end of February, 110,07 EUR were still invested there with an IRR of 10,22%.

If you are interested in LendSecured, you can use my link* and get 1% cashback for 180 days. I will receive 10 € for the successful registration and also 1% cashback for 180 days.

Withdrawal phase

Crowdlending

![]()

In February there was 81,49 EUR in interest. My ratio, the delayed projects, decreased neatly compared to the previous month, but still high at 55%. At the end of the month my investment was still 13.644 EUR with an IRR of 8,69%.

Further, because of the risk of the platform and projects, 50% of the investment is ‘questionable' to me (regardless of the ~55% delayed projects). Especially due to the Corona pandemic, which will have a massive effect on tourism and restaurants.

With my link* there is 1% cashback for 180 days! I receive 1% too + one-time 10€.

Investment expires

![]()

The British platform AxiaFunder offers investing in an area I haven't seen before because they offer investing in litigation cases. You can find an interview with CEO Cormac Leech at explorerp2p.com. Very worth reading!

My initial investment was £500. Yes, that's the minimum investment and a lot. You have to bring some capital with you in order to have proper diversification. The same is also possible for a total loss, and even a loss of more than the invested money. My test project is still floating in the air (I'm not allowed to give more details). On the positive side returns of 20-30% p.a. are possible. So it's a high risk test balloon! In February the IRR is 4,39% due to currency effects.

I'm therefore letting my investment expire (if possible), because you need a lot of capital for a reasonable diversification. I don't have that and I'm not willing to invest that much there either.

If AxiaFunder is an interesting platform for you, I would be happy if you use my link*. My reward is 30€.

![]()

There were small principal repayments at Crowdestate in February. The complete exit is thus dragging on. The IRR was -7,71% and there are still 152,65 EUR on the account.

Portfolio performance income

Month No. 2 in the new year and I am again above the 300 EUR feel-good limit. A total of 316,49 EUR in interest was paid out to me. Mintos drops a bit due to the strategy change. Reinvest24 shines with successfully repaid projects!

Distribution by P2P/Crowlending classes

Below you can find my distribution between the individual P2P / crowdlending classes for February.

- 38,15% (P2P (Buy-back)

- 28,85% Crowdlending

- 0,83% P2B

- 25,86% P2B (Real estate)

- 2,94% P2P

- 2,11% P2P (Short-term)

- 1,26% Misc. (AxiaFunder)

Affiliate/referral income

I would say that I'm one of the most transparent bloggers when it comes to affiliate and referral income. Therefore, there is also pure transparency for February. 122,12 EUR were affiliate revenues distributed over four platforms.

Nevertheless, there was referral income from the following platforms:

- Quanloop*: 22,07 €

- Reinvest24*: 1 €

Summary

In February, the focus was on Russia's invasion of Ukraine, and of course it still is. Just terrible… To support Ukraine, some platforms offer donation projects and I can only appeal to every P2P investor to donate. The impact on the individual platforms will probably become more visible in the coming months. But for me it was clear to immediately kick all Russian and Belarusian loan providers out of Auto-Invests. I also removed the Ukrainian loan providers and some Moldovan and Kazakh ones (because of Russian bank connections etc.).

I hope you found my summary interesting as always. I'm always open for constructive criticism and suggestions. Follow me on Instagram. There I post not only about P2P and crowdlending, but also about stocks, dividends and options. So have a look! That's it for today's post, see you again at the P2P portfolio update for March. Stay healthy!

Feel free to let me know in the comments how your P2P investments are going or which platforms you have worries and concerns about!

About new projects on Twitter, Instagram and Facebook

On my own behalf, I would like to mention that I also present new projects on Twitter (kaph1016) and Instagram (investdiversified) in which I invest myself. Also, on Facebook I have a page. There are also a few insights into how I invest in other areas. So just follow me :).

*Some links in my posts are affiliate or referral links. That means I get a little bonus. For each of those who use these links, however, there are no costs or other disadvantages. On the contrary, there is usually a start bonus or cashback. So if you use these links, you support my blog and for that I say thank you in advance!