Hello everyone! It's been an unusually long time without anything to read in the P2P sector. But that changes now. With today's blog post, I'm bringing you the P2P portfolio update June 2023. Enjoy reading!

‘Strategy'

Since the last Portfolio update in November 2022, not much has changed. I still have a total of around 45.000 EUR invested across various platforms. As I continue to build up equity for a property, I withdraw the interest from most platforms (except for some where the fees make it not worthwhile). However, in the past few months, I have reduced or completely withdrawn from a few platforms. As usual, I'll provide an overview using the IRR ranking and then discuss each platform in detail. I won't include a table anymore, as it's time-consuming to update it every month. I will also skip the categories “Will be reinvested” and “Withdrawal phase” since interest is regularly deducted from all platforms. I will only mention the category “Investment expires” to inform about relevant platforms.

IRR ranking June 2023

I've selected the 01.07.2017 as a start, as this is where I started tracking my P2P investments.

- Lendermarket 18,12%

- Quanloop 18,06% ***

- hive5 15,08% ***

- Afranga 12,93%

- Esketit 12,71%

- NeoFinance 12,64%

- Robocash 11,90%

- Viainvest 11,77%

- Income Marketplace 11,69%

- Bondster 11,26%

- Twino 10,87%

- IUVO 10,72%

- PeerBerry 10,68%

- Lande 10,33%

- Mintos 10,32% **

- ReInvest24 9,24% **

- EstateGuru 8,92%

- Debitum Network 8,68%

- Crowdestor 7,72% **

- Linked Finance 7,53%

- Bulkestate 7,22% *

- InRento 7,00% **

- Go & Grow 6,58%

- EvoEstate 6,23% */**

- AxiaFunder (GBP) 1,58% */****

- Bullride -3,37% **/***

Bondora API 19,99%Swaper 13,41%Moncera 9,22%Crowdestate -7,31%

The * and colors have the following meanings:

- * Investment (temporarily) paused

- ** Fees (on primary or secondary market)

- *** Test balloon

- **** Currency fluctuations

xxxxInvestment stopped/finished successfully- Green Yield in line or above expectations

- Yellow Yield could be better

- Red Platform underperforms

Platforms

P2P (Buy-Back)

![]()

Lendermarket remains the strongest platform in my P2P portfolio in terms of returns. This is due, among other things, to the generally high interest rates, and there are also cashback campaigns from time to time. As of the end of June, the IRR was 18,12% with an investment of 1.624 EUR. The platform has a new CEO, Conor Gibney, and is currently seeking a license in Ireland.

Since I have ‘only' invested a little over 1.000 EUR in Lendermarket, my investment doesn't feel as exposed as the rest.

If you use my link*, you can get up to 5% cashback through the current Summer Cashback campaign when you invest 1.000 EUR or more. The campaign has been running since July 14, 2023, for 5 weeks! I will receive a one-time 5€ + 1,5%. You can find the exact conditions here.

![]()

At Robocash, I had invested 770,08 EUR at the end of June, and the IRR was 11,90%. I believe I will reach the 1.000 EUR investment mark before long.

Due to the still relatively low investment amount, I don't see my investment as questionable. Additionally, Robocash has a long track record, which adds to my confidence in the platform.

If you are interested in Robocash, you can use my link*. As compensation, I get 1% cashback after 90 days and a one-time 5€.

![]()

I have withdrawn some funds from Mintos in the last few months! In April, I had to write off around 60 EUR for about two-thirds of my outstanding claims from Revo Technology. The IRR at Mintos was 10,32% at the end of June, with an investment of 5.956 EUR. I have been investing manually and selectively on the platform for a long time, especially focusing on loans from the following loan originators:

- DelfinGroup

- Eleving Group

- IuteCredit

- Credifiel

- Everest Finanse

- Sun Finance

Mintos is one of my largest platforms. Nothing has changed with the questionable investments; they still account for around 38% of my portfolio, specifically those under “in Recovery.

Mintos* offers until August 31, 2023 a 50 EUR bonus for an investment of at least 1.000 EUR and on top 1% cashback for 90 days. I receive 50 EUR, too.

At IUVO, I have been gradually reducing my investment since the beginning of the year. I have invested around 1.569 EUR with an IRR of 10,72%. I am waiting for further information regarding the planned restructuring at CBC.

At IUVO, 27% of my investments are questionable due to the Polish CBC loans.

By registering by clicking on the banner above, I will receive a one-time 5€ upon registration and 2% of the investment of the first 30 days and 3% for investments from day 31-90.

Twino is running smoothly again, but it is still quite annoying when trying to track interest and withholding tax properly. However, the reporting is not only Twino's concern. The IRR at Twino stands at 10,87% with an investment of 1.219 EUR. The repayment of Russian loans is not looking very promisin

The platform has been running solidly for almost 4 years, and I don't consider my investment questionable (anymore). However, all Russian loans are logically considered questionable.

You can register for Twino* using my link, which offers a much better deal for you. If you invest 500€, we both receive a bonus of 20€.

Afranga continues to run smoothly, doing what it's meant to do – generate interest. At the end of June, I had invested 678,40 EUR with an IRR of 12,93%. Afranga is one of the platforms from which I occasionally withdraw a few euros.

As I haven't invested a significant amount, I don't consider my investment questionable. Sooner or later, I will increase my investment on the platform.

If you are interested in Afranga, you are welcome to use my link* and support my blog. Unfortunately, only I receive 1% cashback. Prerequisite for this, you invest >500 EUR.

Esketit has slightly lowered its interest rates in recent months, likely due to the high demand for the platform. At the end of June, I had invested 620,07 EUR with an IRR of 12,71%. There is also a new loan originator, Aksioma 24, which is now part of the “Diversified” Auto-Invest strategy. If you have set up this strategy, you may need to adjust it accordingly.

Similar to Afranga, I consider my investment at Esketit as non-questionable. The platform has established itself, and due to the small investment amount, I don't see it as exposed. In a few months, I plan to increase my investment.

For the curious, Esketit offers 1% cashback on the investment for the first 90 days at Esketit with my link*. I also receive this as compensation + one-time 5€.

At Income Marketplace, I had invested 556,95 EUR at the end of June, with an IRR of 11,69%. The Brazilian loan originator ClickCash did not perform buybacks as planned at the end of last year, and repayments have been slow, as mentioned on the Income Marketplace blog. In February, an “Early Buyback” feature was introduced, which may be useful for long-term loans. The buyback needs to be manually triggered in such cases.

Income Marketplace is now established, but the situation with ClickCash needs to be monitored. Nonetheless, I don't consider my investment questionable.

If you want to test the platform there is 1% cashback for you if you use my link* and use the code CLHOFU during registration. I receive 1% too + one-time 20€.

![]()

At Peerberry, things have been improving steadily. Over the past 15 months, a remarkable 77% of loans at risk due to the war have been recovered, amounting to approximately 39 million EUR. The XIRR at the end of June was 10,68% with an investment of 1.118 EUR.

One of the most solid platforms for over three years! Here, too, until now. Still, a war is a worst case scenario, which is why about 55,3% of my portfolio is questionable, despite the redemptions so far.

A while ago PeerBerry introduced a loyalty bonus, but with high requirements:

- 0,5% for 10.000€

- 0,75% for 25.000€

- 1% for 40.000€

If you use my PeerBerry* link, I'll receive 5€ + 1% from investments for 60 days.

![]()

In my allusion to the need for improved reporting at Twino, I was referring to platforms like Viainvest as well. Having to download a PDF every time, well, I think that could be done better. Viainvest now offers auto invest strategies. My IRR stood at 11,77% by the end of the month with an investment of 1.689 EUR.

In my opinion, Viainvest is quite reliable, and therefore, I do not consider my investment questionable.

If you register at Viainvest* I will get 10€ one-time and 1% cashback for 90 days.

P2P

![]()

NeoFinance was one of the platforms where I had slightly reduced my investment overall. Currently, there is still 1.202 EUR invested with an IRR of 12,64%.

The platform's calculated return is 13,99%, with a deduction of 15% withholding tax (which can be reduced to 10%).

At least the loans that are more than 90 days overdue need to be considered questionable, even though they might pay in the future. Therefore, approximately 19% of the total investments are considered questionable.

NeoFinance* changed and lowered their offer too. There is 1% cashback for you and me for 90 days.

P2B (Real estate)

![]()

By the end of June, the IRR at Reinvest24 was 9,24% with an investment of 2.569 EUR. My three projects in Moldova and a business loan (Interchem) are currently significantly delayed. The strategic partnership with Kirsan is more or less terminated, so I'm curious about the fate of those specific projects. I think it will be a long battle. However, there has been a new strategic partner announced with Shojin. I always thought they were a reliable platform 🙂 Just kidding!

Reinvest24 is already over 5 years old! As of today, my Moldovan projects are considered questionable.

If you want to invest on ReInvest24*, there is a bonus of 10 EUR running for new investors! I receive 1% cashback.

InRentos' weight in my P2P portfolio continues to grow slowly. Every month, the interest from EvoEstate is automatically transferred to InRento, and I invest once the minimum investment amount of 100 EUR is reached. The IRR at the end of June was 7% with an investment of 1.100 EUR. So, my 1.000 EUR target has already been achieved, and for now, I prefer to withdraw incoming funds from EvoEstate. InRento could also improve their reporting!

I don't consider my investment of just over 1k as questionable so far.

You can register via my InRento* link, for this you will receive a 20€ bonus, while I will receive 20€, too.

![]()

EstateGuru has become one of the problematic cases in my P2P portfolio in recent months. The reason for that is primarily the German projects, which are all in default now. EstateGuru now communicates the developments with these projects quite transparently via email, and many investor questions have been answered. However, the recovery process in Germany is known to take longer than in other countries. By the end of June, 3.361 EUR were invested in EstateGuru with an IRR of 8,92%. I also withdrew some free funds from here.

About 40% of my invested capital, everything that is “In default,” I consider questionable. So far, I have not experienced any capital losses with EstateGuru. I am optimistic that it will stay that way.

At EstateGuru* there is a 0,5% cashback for 3 months. I also receive the cashback and in addition 5€.

P2B

![]()

I recently re-entered Debitum. I reported on the reasons in the blog post. I invested 100 EUR, and the “old” IRR was 8,28%.

I re-entered with 100 EUR and will gradually increase my investment. Due to the small amount, I do not consider the investment questionable.

If you want to invest in Debitum Network*, there is an exclusive offer for you. If you register through my link*, you will receive a 1% bonus when you invest from 10 EUR in ABS with a minimum maturity of 90 days. If you invest in Sandbox Funding, you will get 2% cashback! I will receive a one-time 10 EUR and 2% cashback for 90 days on the investment.

![]()

With hive5, I added another platform to my portfolio at the end of September. In the interview with CEO Ričardas Vandzinskas you can learn more about the Lithuanian platform based in Croatia. Currently, I can report an IRR of 15,08% with an investment of 222,50 EUR.

I initially consider new platforms as test ballon for about a year. After that, I decide whether to increase the investment or not.

If you use my link*, I will receive a one-time 10€ and 2% cashback.

![]()

Quanloop had an investment of 81,70 EUR by the end of June, with an IRR of 18,06%. Even though it has been more than a year since the initial investment, I still treat Quanloop as a test pilot because it is essentially a black box. Currently, I am researching for a deep dive into it.

The experiment will continue, but without further investments.

If you still want to take the increased risk with Quanloop, you will receive a 5€ bonus with my link*. I receive 2.5% cashback.

![]()

LinkedFinance has an IRR of 7,53% by now. The investment stands at 529,34 EUR.

So far, I have only had paying or already repaid projects. Therefore, I do not consider my investment questionable.

Linked Finance doesn't have an affiliate program, so there's nothing for you or me. Nevertheless, you can register here if you like.

P2P (Short-term)

![]() Go & Grow

Go & Grow

Go & Grow I mainly use for a small part of my cash and will also use it for my side hustle and savings for insurance payments. Because of the withdrawals from time to time and the fee of 1 EUR IRR is at 6,58%. In June there are still about 18 EUR left on the account.

I do not consider an investment in Bondora to be questionable.

A 5€ bonus is available for you at Bondora* right after registration.

Crowdlending

![]()

At Lande, I currently have an investment of 281,57 EUR with an IRR of 10,33%. The platform, with investment opportunities in land, machinery, and seeds, provides good diversification, and I plan to gradually increase my investment to around 1.000 EUR.

If you are interested in Lande, you can use my link* and get 1% cashback for 180 days. I will receive 10 € for the successful registration and also 1% cashback for 180 days.

Misc.

![]()

I have been invested in Bullride for over a year now. In the April 2022 portfolio update, I introduced the platform. As of now, the whole investment is definitely NOT a good one. Including the write-offs, my IRR is -3.37%. We will see if this turns around, but that's exactly why this is an experiment, even with more investment than usual.

For a test balloon, this is a very high amount, and it is 100% questionable until the first results come in.

If you register with my link* you will get 10€ and 1% cashback for 90 days.

Investment expires

![]()

I have been receiving interest payments from Crowdestor in the past months, but never exceeding 20 EUR. The previous month had a similar level. My indicator, the late projects, has increased further compared to the last portfolio update, reaching 67%. This was also due to some smaller projects that were repaid. By the end of the month, the investment was still 11.647 EUR with an IRR of 7,72%.

Due to the platform and project risks, 50% of my investment is questionable (independent of the ~67% late projects).

Last year, I expressed my dissatisfaction with Bondster regarding the Mikrokasa loans (which are still not officially considered defaulted) and mentioned that I might take action. Since then, I have indeed reduced my investment from around 1.200 EUR to the current 714,07 EUR. If possible, I will withdraw everything. The IRR at the end of the month was 11,26%.

Due to the “defaulted” Polish loans, I consider 30% of the investment questionable

![]()

EvoEstate had 4.161 EUR invested by the end of June with an IRR of 6,23%. The calculated return differs significantly from the “Net Annual Returns” of 10,73% due to the end-of-term projects.

All returns from EvoEstate are initially automated to be transferred to InRento. When there are new projects there, I invest, and excess funds are withdrawn.

![]()

The British platform AxiaFunder offers investing in an area I haven't seen before because they offer investing in litigation cases. You can find an interview with CEO Cormac Leech at explorerp2p.com. Very worth reading!

My initial investment was £500. Yes, that's the minimum investment and a lot. You have to bring some capital with you in order to have proper diversification. The same is also possible for a total loss, and even a loss of more than the invested money. My test project is still floating in the air (I'm not allowed to give more details). On the positive side returns of 20-30% p.a. are possible. So it's a high risk test balloon! In June the IRR is 1,58% due to currency effects.

I'm therefore letting my investment expire (if possible), because you need a lot of capital for a reasonable diversification. I don't have that and I'm not willing to invest that much there either.

If AxiaFunder is an interesting platform for you, I would be happy if you use my link*. My reward is 17,50€ and 3% Cashback.

![]()

Since November 2022, there have been no further repayments at Crowdestate. The complete exit is still ongoing. The IRR was -7,03%, and there are still 150,05 EUR in the account.

![]()

At the end of June, 839,18 EUR were invested at Bulkestate, with an IRR of 7,22%. Repayments are scarce, and information is also limited. Regarding withdrawals, you often have to send emails to ensure they are processed. Beware!

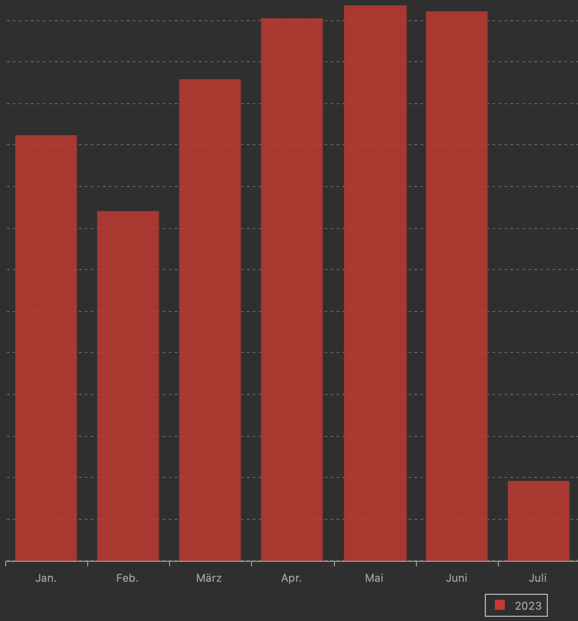

Portfolio performance – interest

Interest:

- December '22: 206,88 EUR

- January: 204,42 EUR

- February: 168,15 EUR

- March: 231,27 EUR

- April: 260,86 EUR

- May: 266,77 EUR

- June: 264,33 EUR

Note: Each month includes an interest charge of 45,83 EUR due to the write-off (for tax reasons) of the two Bullride e-scooters.

In the above list or screenshot, you can see the interest income from my P2P portfolio in recent months. I haven't been able to reach my comfortable threshold of 300 EUR for quite some time, and it will likely be challenging to achieve that in the near future.

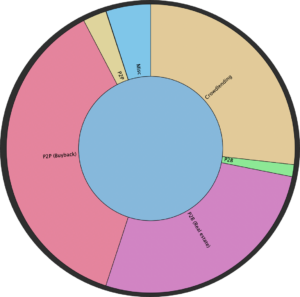

Distribution by P2P/Crowlending classes

To conclude, I will show you the distribution of my investments in various P2P/Crowdlending classes in June.

- 37,28% (P2P – Buy-back)

- 26,75% Crowdlending

- 1,66% P2B (Peer-to-Business)

- 26,90% P2B (Real estate)

- 2,49% P2P (Peer-to-Peer)

- 0,04% P2P (Short-term)

- 4,89% Misc. (Bullride, AxiaFunder)

Affiliate/referral income

I would say that I am one of the most transparent bloggers when it comes to affiliate and referral income. Therefore, I provide complete transparency for the past months as well.

Affiliate Income:

- January: 272,07 EUR

- March: 71,75 EUR

- May: 273,21 EUR

Referral Income:

- December '22: Quanloop* 21,02 EUR, Reinvest24*: 1,10 EUR

- January: Quanloop* 22,58 EUR

- February: Quanloop* 22,97 EUR

- March: Quanloop* 20,78 EUR

- April: Quanloop* 20,87 EUR

- May: Quanloop* 21,93 EUR

- June: Quanloop* 23,99 EUR

My P2P tools

- P2P Platform Rating Premium from Lars Wrobbel*

Since more than two years Lars regularly publishes his platform rating. This is now available in a free version as well as a premium version. Advantage of this is the data access to ALL platforms! The table is constantly updated, update via Telegram when there are changes in the rating and there are extended comments and sources. The whole thing runs 12 months for 59 € (no subscription!). If you use my link*, you get a bonus month!

About new projects on Twitter, Instagram and Facebook

I hope you found my summary interesting as always. I'm always open for constructive criticism and suggestions. Follow me on Instagram (or Twitter and Facebook). There I post not only about P2P and crowdlending, but also about stocks, dividends and options. So have a look! That's it for today's post, see you again at the P2P portfolio update for October. Bye!

Feel free to let me know in the comments how your P2P investments are going or which platforms you have worries and concerns about!

*Some links in my posts are affiliate or referral links. That means I get a little bonus. For each of those who use these links, however, there are no costs or other disadvantages. On the contrary, there is usually a start bonus or cashback. So if you use these links, you support my blog and for that I say thank you in advance!