Hello, friends of cash flow! With the P2P portfolio update December 2021, I would like to officially close the P2P year 2021. December followed the previous months and brought a lot of interest. Since one goal for 2022 is to massively increase the P2P area, hardly any interest will be paid out now, but redistributed at most. You can read which platforms this affects in the following blog post. Have fun!

First comes the IRR ranking, as usual, and then a closer look at the individual platforms. I have adjusted the subdivision of the platforms once again because it has led to confusion here and there. There are the categories ‘(Re)invested‘, ‘Withdrawal phase‘ and ‘Investment expires'.

‘Strategy'

My strategy for 2022 will be adjusted to the extent that the cash flow from interest on the platforms will remain or at least only be redistributed within the platforms. The goal is to increase the investment on as many platforms as possible to such an extent that I can receive 25 EUR in interest every month (if I want to!).

IRR ranking December 2021

I've selected the 01.07.2017 as a start, as this is where I started tracking my P2P investments.

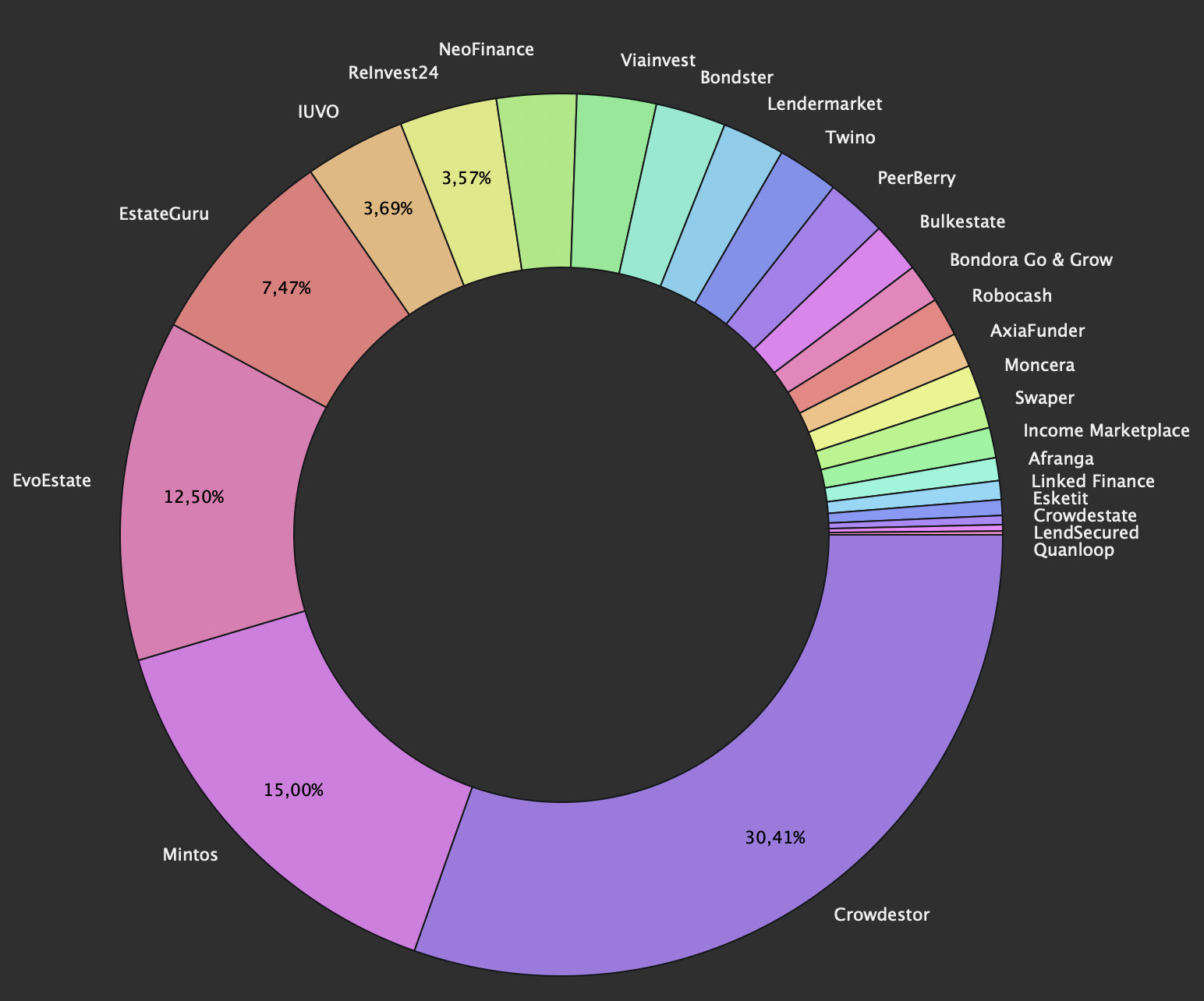

Platform | Initial investment | IRR (%) | Change previous month (%) | Invested (EUR) | Change previous month (EUR) |

|---|---|---|---|---|---|

19.07.2017 | 12,20 | -0,17 | 7086 | +34 | |

30.10.2017 | 10,93 | -0,02 | 1059 | -1 | |

09.11.2017 | 6,66 | -0,03 | 673,88 | +2,29 | |

14.05.2018 | 12,66 | -0,04 | 1049 | +10 | |

31.07.2018 | 11,87 | -0,08 | 1744 | +12 | |

11.08.2018 | 12,72 | -0,01 | 535,57 | +5,30 | |

01.02.2019 | 9,81 | -0,04 | 3530 | +24 | |

14.02.2019 | 13,18 | -0,03 | 1380 | +14 | |

20.02.2019 | 7,61 | -0,09 | 1686 | +64 | |

21.03.2019 | 8,75 | +0,20 | 14366 | +59 | |

30.03.2019 | 11,37 | -0,04 | 1215 | 0 | |

12.04.2019 | 11,66 | 0 | 1370 | +3 | |

17.05.2019 | 8,70 | +1,18 | 877,47 | -29,61 | |

Crowdestate | 20.05.2019 | -7,80 | +0,05 | 168,25 | 0 |

31.07.2019 | 3,05 | +0,07 | 5904 | -36 | |

15.02.2020 | 15,80 | -0,30 | 1082 | +10 | |

20.02.2020 | 7,29 | +0,03 | 326,43 | +2,10 | |

29.05.2020 | 4,47 | +0,68 | 587,11 | +6 | |

22.07.2020 | 9,90 | +0,02 | 573,20 | +4,66 | |

28.01.2021 | 11,36 | -0,06 | 109,33 | +0,95 | |

21.03.2021 | 15,33 | +0,19 | 395,19 | +5,14 | |

10.06.2021 | 13,38 | +0,32 | 270,85 | +3,23 | |

10.06.2021 | 10,30 | +2,09 | 669,70 | +8,36 | |

23.07.2021 | 10,75 | +1,82 | 523,04 | +7,58 | |

15.11.2021 | 18,29 | -0,63 | 63,77 | 0 | |

31.12.2021 | +0,98 | +0,33 | 47244 | +205 |

Platforms

(Re)investing

Currently, I'm in a kind of withdrawal phase or consolidation / reallocation. On the following platforms, however, I continue to reinvest and plan to increase the investment moderately in some cases.

P2P (Buy-back)

![]()

In the last P2P portfolio update, I reported that I switched from individual auto investments per loan originator to the predefined strategies on Mintos. This was partly to save time, as interest rates have fallen so much anyway that separate AIs are not worthwhile. Especially since they have to be adjusted regularly. On the other hand, it has the advantage that I'm relatively quickly liquid, which is given by the conservative strategy. Of course, there is one disadvantage: the interest rate is even lower. The IRR at the end of December was 12,20% with 7.086 EUR invested. I also plan to increase my Mintos investments.

Even if Mintos is one of my largest platforms, still 18,2% of my investment is questionable. Namely all pending payments and loans in recovery.

From October 4, 2021 Mintos* changes its affiliate program and introduces a waiting list for new investors. I receive 6€ if you use my link* for registration.

There was no news at IUVO in December. 1.744 EUR with an IRR of 11,87% are invested.

Marking 10% of the capital as questionable seems to be appropriate because of the amount of HR loans.

- For IUVO there are two different offers. Unfortunately, the referral program is extremely unattractive since a few days. For the first you can contact me because unfortunately it has to be done manually, and I have to invite you. You get 1,5% cashback for investment above 1.000€. I receive 1,5% too.

- With the 2nd offer (click on the banner) I get 5€ and 2% of the investment in the first 30 days and 3% for the investment of day 31-90

Besides the audited annual report, which you can find here, something has actually changed at Lendermarket. New colors came into play, red was replaced by purple. Of course, this has not affected my performance, which at the end of December was an IRR of 15,80% with an investment of 1.082 EUR.

Because the platform is new and I ‘only' invested 1.000 EUR I won't put capital as questionable for now.

On the platform you get 1% cashback if you are using my link*. Currently, in total up to 16%! My reward is 5€ onetime + 1,5%

![]()

On the transparency front, of course, little has changed. But the numbers are still right. At the end of December, the IRR was 12,72%. All this with an investment of 535,57 EUR.

Because I just have a few Euros invested, I won't put it as questionable for now.

If you use my link* my reward is onetime 5€ + 2% cashback for 90 days.

The IRR at Twino was 10,93% in December with 1.059 EUR invested. At the beginning of the month, another 10 EUR in interest was deducted. It is interesting that Twino also wants to open up India as a market in the future! This can be seen in the vacancies, where, for example, a COO is being sought.

So far, the platform has been running so solidly for almost 4 years that I don't consider my investment questionable.

Here* you can register. If you invest 100€ we both are rewarded with a bonus of 15€.

At Moncera, 573,20 EUR was invested at the end of December with an IRR of 9,90%. So we remain at just under 10%.

I'm watching the platform very closely, but so far I have no reason to consider my investment questionable. Nevertheless, the platform is of course very young.

If you use my Moncera link* we both receive 0,5% cashback on all deposits made by you in the first 60 day.

With Afranga, the biggest problem is actually the cash drag, as quite a lot of investors now want to invest on the platform. My investment at the end of December are 395,19 EUR with an IRR of 15,33%.

As always with new platforms, I test the platform first with a smaller amount and share my observations. In January, I will top up at Afranga. Due to the small investment amount, I don't see the investment as such as questionable.

If you are interested in Afranga, you are welcome to use my link* and support my blog. Unfortunately, only I receive 1% cashback. Prerequisite for this, you invest >500 EUR.

Esketit's performance also looks better every month, with the IRR rising to 13,38% month-on-month at 270,85 EUR invested.

Of course, this is also a test balloon. I'm looking at the whole thing over a longer period of time before I increase the investment much, however, it's also time for some more skin-in-the-game with Esketit in January. Due to the low investment sum, I do not see the investment as such as questionable.

For the curious, there is 1% cashback on the investment for the first 90 days at Esketit with my link*. I also receive this as compensation + one-time 5€.

![]()

The 400 EUR freshly invested in November are working diligently at Robocash to bring me more interest. At the end of December 669,70 EUR were invested in the account with an IRR of 10,30%.

Due to the increase, but still a small investment amount, I do not see the investment as such as questionable.

If you are interested in Robocash, you can use my link* and support my blog. As compensation, I get 1% cashback after 90 days and a one-time 5€.

In the interview with CEO Kimmo Rytkönen you can learn more about the platform, otherwise Income Marketplace runs completely silent. Recently, a fifth loan provider was added, namely the Indonesian company Danarupiah, which is also known from other platforms. These loans have an interest rate of 12% and the junior share is 35%. As a reminder, besides repurchase obligation, Income Marketplace has a second safety net with the cash flow buffer. Therefore, I will only invest in Danarupiah loans through this platform. The investment at the end of December was 523,04 EUR with an IRR of 10,75% on.

500€ is of course not a small amount for a test balloon, but without some skin-in-the-game experience reports are not authentic.

If you want to test the platform there is 1% cashback for you if you use my link* and use the code CLHOFU during registration. I receive 1% too + one-time 20€.

P2B (Real estate)

![]()

At EstateGuru, it can be observed that interest rates are now falling a little more. However, this is still alright overall. At the end of December, 3.530 EUR were invested with an IRR of 9,81%. EstateGuru also has a small novelty to offer, because there are now three strategies available that start at 50 EUR. I chose the custom variant.

I don't consider my invested capital to be ‘questionable'. So far EstateGuru has always ensured recovery.

At EstateGuru* there is a 0,5% cashback for 3 months. I also receive the cashback and in addition 5€.

![]()

In December, I also added more projects. Further increases are planned! The IRR was 7,61% at the end of December with 1.686 EUR invested. Soon Reinvest24 will be one of the top 5 platforms in my P2P portfolio.

I consider 10% of my investment as questionable, as ReInvest24 is still a young platform.

If you want to invest on ReInvest24*, there is a 10€ bonus for you. I'll receive 1% of the investment.

![]()

At the beginning of December, I withdrew some free capital, but that was only 57 EUR. In total, 5.904 EUR is still invested in EvoEstate at the end of December with an IRR of 3,05%. By the way, the calculated return deviates strongly from the ‘Net Annual Returns', which is 11,12%, due to final maturity projects.

Although, EvoEstate is still one of the younger platforms. I don't (any longer) consider my capital to be questionable.

For EvoEstate there is a 0,5% cashback for 6 months with this link*. I get 0,5% too and one-time 5€.

P2B

![]()

I only restarted Quanloop in November. In the following month of December, 63,77 EUR continued to work there, I deactivated the payout mode again and am now reinvesting again for the time being. Due to the earlier investment, the IRR is at 18,29%, but should quickly fall to a normal level.

I'm sort of continuing the experiment, only with a bit more cash, in the medium term I had in mind 500-1.000 EUR. And of course I will report about everything.

If you register with Quanloop via my link*, you will receive a bonus of 5€. I get 2,5% cashback.

![]()

There is nothing new to report from Ireland. LinkedFinance continued to perform well in December with an IRR of 7,29% and a total investment of 326,43 EUR. When I see more projects being posted again, I plan to increase the investment there up to 1,000 EUR.

So far, exclusively paying or already repaid projects. Therefore, I do not consider my investment questionable.

Linked Finance doesn't have an affiliate program, so there's nothing for you or me. Nevertheless, you can register here if you like.

P2P

![]()

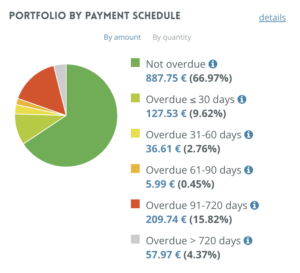

With NeoFinance, things are also running smoothly so far, the red credits are at least no longer increasing that much. At the end of December 1.380 EUR are invested in NeoFinance and the IRR is 13,18%. I don't count the red credits as defaults so far, since they do make a payment from time to time. The manually selected loans have very strict criteria. Since I have been doing this specifically, the number of loans that are up to 90 days late has felt to be declining somewhat. However, I have yet to back up this observation with numbers. NeoFinance is one of the platforms where I have not paid out any interest, as there is a withdrawal fee. In the following screenshots, a comparison of November 2021 and December 2021.

The return calculated by the platform is now 14,34% after an adjustment of the calculation. There is a deduction of 15% withholding tax (can be reduced to 10% by the way).

At least the 91-270 days overdue loans I have to mark as questionable even though some of them might pay in the future. I think approx. 19% of the capital is questionable in the current situation.

NeoFinance* changed and lowered their offer too. There is 1% cashback for you and me for 90 days.

P2P (Short-term)

![]() Go & Grow

Go & Grow

Go & Grow I mainly use for a small part of my cash and will also use it for my side hustle and savings for insurance payments. Because of the withdrawals from time to time and the fee of 1€ IRR is at 6,66%. At the end of December, there was 673,88 EUR there, part of which I will probably need in January.

I don't think my investment here is in question. Bondora has enough leverage.

A 5€ bonus is available for you at Bondora* right after registration.

Crowdlending

LendSecured is one of the smallest investments, which is about to change. At least 500 EUR should work there and earn interest. That is still the plan, but the free funds are missing. At the end of the month, 109,33 EUR were invested there, with an IRR of 11,36%.

If you are interested in LendSecured, you can use my link*. I'll receive 10 € for the successful registration + 1% cashback for 180 days.

Withdrawal phase

P2P (Buy-back)

![]()

PeerBerry is quietly running along. I will keep a closer eye on Ukrainian loans in the coming weeks (looming conflict with Russia). My IRR was 12,66% with 1.049 EUR invested. Another 10 EUR in interest was withdrawn here.

One of the most solid platforms for over three years.

A while ago PeerBerry introduced a loyalty bonus, but with high requirements:

- 0,5% for 10.000€

- 0,75% for 25.000€

- 1% for 40.000€

If you use my PeerBerry* link, I'll receive 5€ + 1% from investments for 60 days.

Bondster now also has a new color setting, including a logo. At the end of December, the IRR was at 11,37% with 1.215 EUR invested. Here, too, another 10 EUR in interest was withdrawn.

I still see Bondster as a young platform and even if the collection of Polish loans works out very well, I see 30% of the investment as questionable.

There is a 1% cashback after 30 days at Bondster*. I receive 2%.

![]()

Viainvest does what it is supposed to do. The IRR was 11,66% on an investment of 1.370 EUR. Like Bondster and Peerberry, Viainvest I withdrew also 10 EUR in interest. This practice will change in January.

In my opinion, Viainvest is quite solid and so 0% of my capital is questionable (so far).

For the start at Viainvest* there is a 15€ bonus. For this only 50€ need to be invested. I'm also rewarded with 15€ if you register with my link.

P2P (real estate)

![]()

Yes, what can I say about Bulkestate. The new design came in December, but there is not much more transparency and a better overview of repayments, partial payments etc. with it. 877,47 EUR are invested, maybe … or maybe more or less. The IRR was 8,70% at the end of December.

I think about 5% of the capital is questionable, because of the two delayed projects and because I do not know how well the recovery is working.

If you use my link* I'll receive 1% cashback for 180 days and one-time 5€.

Crowdlending

![]()

Interest income in December was once again slightly higher than in the previous months, at 157,43 EUR. My key figure, the delayed projects, is rising 60% due to further successful repayments of smaller projects. My investment at the end of December was 14.366 EUR with an IRR of 8,75%.

Further, because of the risk of the platform and projects, 50% of the investment is ‘questionable' to me (regardless of the ~60% delayed projects). Especially due to the Corona pandemic, which will have a massive effect on tourism and restaurants.

With my link* there is 1% cashback for 180 days! I receive 1% too + one-time 10€.

Investment expires

![]()

The British platform AxiaFunder offers investing in an area I haven't seen before because they offer investing in litigation cases. You can find an interview with CEO Cormac Leech at explorerp2p.com. Very worth reading!

My initial investment was £500. Yes, that's the minimum investment and a lot. You have to bring some capital with you in order to have proper diversification. The same is also possible for a total loss, and even a loss of more than the invested money. My test project is still floating in the air (I'm not allowed to give more details). On the positive side returns of 20-30% p.a. are possible. So it's a high risk test balloon! In December the IRR is 4,47% due to currency effects.

I'm therefore letting my investment expire (if possible), because you need a lot of capital for a reasonable diversification. I don't have that and I'm not willing to invest that much there either.

If AxiaFunder is an interesting platform for you, I would be happy if you use my link*. My reward is 30€.

![]()

In December, there were some redemption payments at Crowdestate, but nothing more. The complete exit is therefore dragging on. The IRR was -7,80% at the end of November and there are still 168,25 EUR on the account.

Portfolio performance income

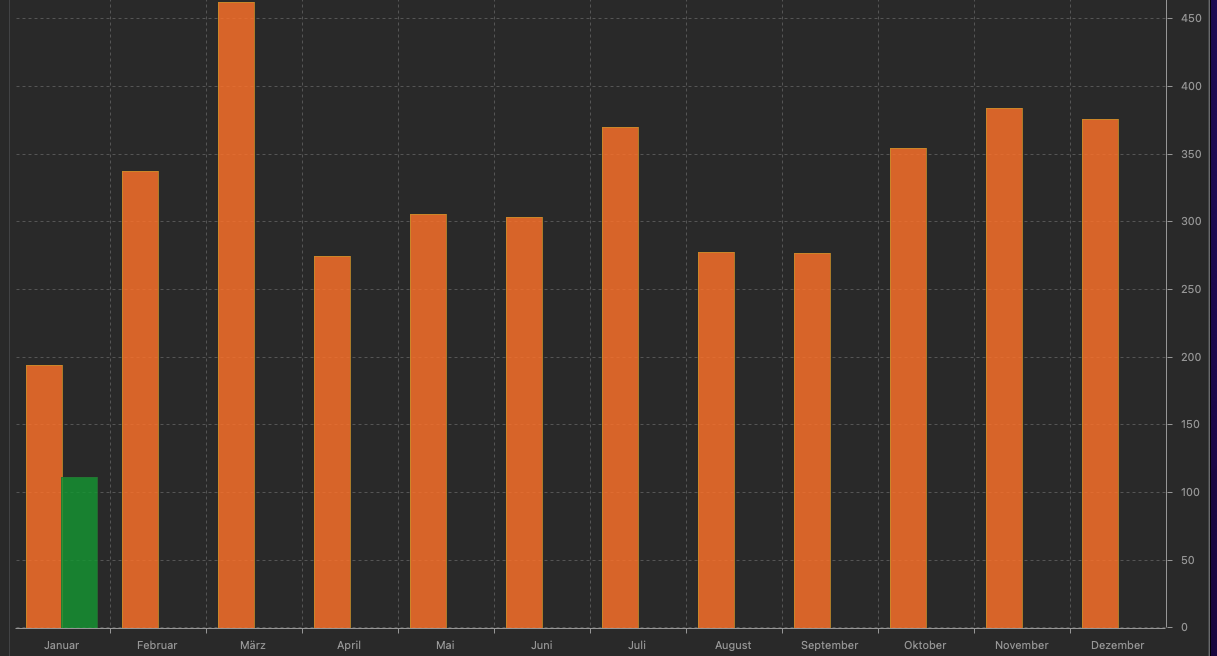

After 355,66 EUR in October and 383,97 EUR in November, December brought another whopping 375,99 EUR. With 157,43 EUR , Crowdestor again had a larger share. At Mintos, the switch to the conservative strategy was already noticeable.

In total, I was able to earn around 3.915 EUR in interest in 2021. This is decent, but it should be significantly increased in 2022 and, above all, stabilize the cash flow!

Affiliate/referral income

I would say that I'm one of the most transparent bloggers when it comes to affiliate and referral income. Therefore, there is also pure transparency for December. Because there was nothing :D.

Nevertheless, there was referral income from the following platforms:

December:

- Quanloop*: 19,21 €

- Reinvest24*: 14,00 €

Summary

With this update, the year 2021 is finally over. The goal I have set myself is to almost double the P2P portfolio to 90,000 EUR in 2022. Of course, that's sporty, but what's the point if you set yourself too low a target. First and foremost, the focus should be on stabilizing and further expanding the cash flow. Alternative investments, which for me include P2P, could bring more returns this year than there is to be earned on the stock markets. At least if you play a pessimistic scenario. But I also want to be prepared for this. More cash flow just reassures! Thanks for reading this far, see you in the January update!

Feel free to let me know in the comments how your P2P investments are going or which platforms you have worries and concerns about!

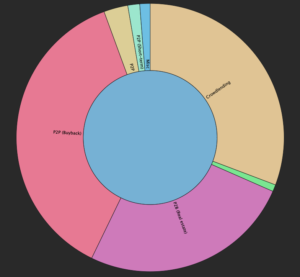

Distribution by P2P/Crowlending classes

Below you can find my distribution between the individual P2P / crowdlending classes for December.

- 37,20% (+-0%) P2P (Buy-back)

- 30,64% (-0,11%) Crowdlending

- 0,83% (+-0%) P2B

- 25,72% (+0,09%) P2B (Real estate)

- 2,92% (+0,01%) P2P

- 1,43% (+-0%) P2P (Short-term)

- 1,26% (+0,01%) Misc. (AxiaFunder)

I hope you found my summary interesting as always. I'm always open for constructive criticism and suggestions. Follow me on Instagram. There I post not only about P2P and crowdlending, but also about stocks, dividends and options. So have a look! We will read about the next portfolio update in September/October.

About new projects on Twitter, Instagram and Facebook

On my own behalf, I would like to mention that I also present new projects on Twitter (kaph1016) and Instagram (investdiversified) in which I invest myself. Also, on Facebook I have a page. There are also a few insights into how I invest in other areas. So just follow me :).

*Some links in my posts are affiliate or referral links. That means I get a little bonus. For each of those who use these links, however, there are no costs or other disadvantages. On the contrary, there is usually a start bonus or cashback. So if you use these links, you support my blog and for that I say thank you in advance!